[ad_1]

Justin Sullivan

The rise of Artificial Intelligence has been a driving force behind tech stocks so far this year, and this trend is unlikely to show any cracks in the foreseeable future with companies of every scale and size wanting to embrace AI in one shape or the other. Broadcom Inc. (NASDAQ:AVGO) has been a direct beneficiary of AI, as the company’s networking solutions have attracted stellar demand for various AI end uses. The increasing demand for cloud data center applications has also led to strong demand for Broadcom’s networking products, paving the way for the company to report robust earnings growth for the fiscal third quarter amid macroeconomic challenges that have dampened the outlook for the chip sector. A closer look at Broadcom’s product portfolio and the industry outlook suggests the company still has a long runway to grow. However, I believe Mr. Market has already rewarded Broadcom handsomely, leaving new investors with no margin of safety to invest in the company today.

Broadcom’s Promising Prospects

My bullish stance on Broadcom’s business stems from two main reasons.

- The encouraging demand environment for Broadcom’s networking segment.

- The diversification benefits expected from the VMware, Inc. (VMW) acquisition.

The networking segment proved to be a driver of Broadcom’s growth in the last quarter, with this segment registering a 20% YoY growth in revenue, helping the company report a 5% YoY growth in total revenue. Networking accounted for 40% of Broadcom’s semiconductor revenue, which highlights the growing importance of this business segment. A closer look at the company’s networking business reveals how this segment is benefiting from the increasing adoption of AI technology.

With the increasing use cases of AI technology, there is a growing demand for data centers to store massive amounts of data. To generate relevant content and support various applications built with AI technology, data centers are forced to invest millions of dollars to upgrade their infrastructure with specialized GPUs and Tensor Processing Units. To scale out AI clusters within data centers, advanced networking technologies are needed, and Broadcom is a key supplier of custom AI compute engines and networking technologies to the data center industry.

The company is aggressively investing in R&D efforts to develop silicon technology to support data centers and to offer low-latency Ethernet technology to fuel machine learning and AI applications. Broadcom is also working on Tomahawk 5 and 6 switches and Jericho3-AI routers with ambitious plans to achieve 800-gigabit connectivity in the near future.

Broadcom’s investments, in my opinion, will help the company maintain its position as a key enabler of AI technology in the foreseeable future. With innovative products, Broadcom seems well-positioned to benefit from the favorable demand environment for networking products.

Broadcom operates under two main business segments today.

- Semiconductor solutions

- Infrastructure software

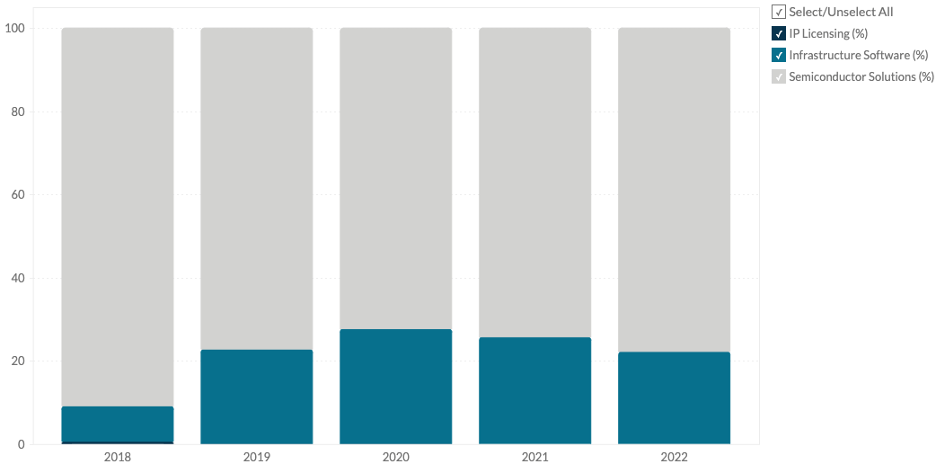

As the below chart illustrates, the semiconductor solutions segment accounts for the bulk of revenue today. In the last few years, the infrastructure software segment has accounted for just over 20% of annual revenue.

Exhibit 1: Broadcom revenue by segment (%)

Business Quant

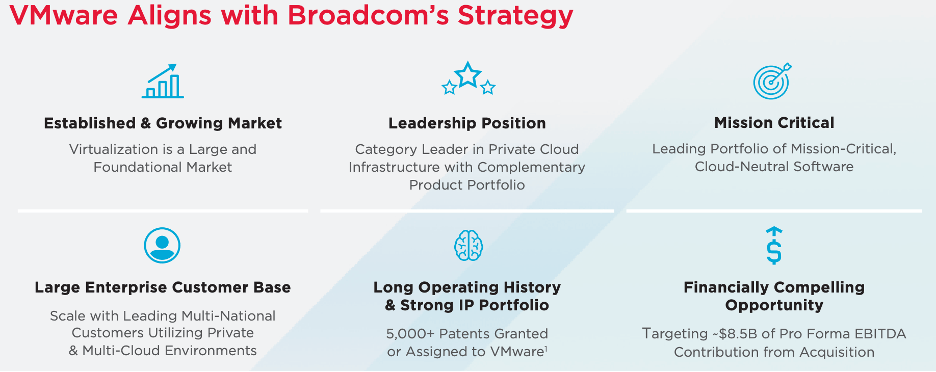

The planned acquisition of VMware will help Broadcom strike a better balance between software and chip revenue as VMware brings with it an established SaaS business. Broadcom is after VMware’s network virtualization portfolio which boasts a sticky customer base. On August 21, the Competition and Markets Authority in the UK approved the proposed acquisition of VMware by Broadcom, removing the biggest regulatory hurdle this deal faced ever since its announcement. The European Union had already approved the deal at the time of CMA’s decision. With no regulatory challenges on the horizon in the U.S., the deal will only face scrutiny in China. Given that this deal does not necessarily consolidate the chip sector, I believe Chinese regulators will give the green light in the coming months, similar to how they approved Microsoft Corporation’s (MSFT) acquisition of Activision Blizzard (ATVI).

The VMware acquisition, in my opinion, will serve two purposes. First, this acquisition will help Broadcom expand its core customer base as VMware’s virtualization and cloud computing products will complement its existing portfolio. The company is likely to find opportunities to cross-sell VMware’s products to existing data center customers, thereby increasing the lifetime value of a customer. Second, VMware will bring in a stable, consistent stream of revenue to Broadcom, helping the company negate some of the cyclicality effects of the semiconductor industry.

Exhibit 2: The case for acquiring VMware

Company presentation

VMware has a strong presence in the cloud infrastructure solutions sector as Virtual Machines and virtualization technology play a key role in the adoption of cloud computing. In many emerging markets, SMEs are beginning to embrace cloud computing, creating new opportunities for Broadcom to use its existing business relationships to drive demand for VMware’s virtualization solutions. According to the findings of Alibaba Group Holding Limited (BABA), 84% of businesses in Asia expect full cloud migration in the next two years, and a similar percentage of businesses are planning to boost their investments in the cloud in the coming year.

Exhibit 3: Cloud investment in Asia

Alibaba

The VMware acquisition is being completed at a time when emerging markets are on the brink of boosting their investments in the cloud, which bodes well for Broadcom.

The VMware acquisition will also establish Broadcom’s appeal as a key infrastructure solutions provider in the cloud computing sector, strengthening its competitive advantages. As a long-term-oriented growth investor, I prefer investing in companies with the potential to enjoy durable competitive advantages, and Broadcom’s appeal as such a company will get a boost once this deal is completed.

Based on the favorable demand environment for the networking segment and the expected diversification benefits and synergies from the VMware acquisition, I believe Broadcom is well-positioned for sustainable growth in the next few years.

AVGO Stock’s Valuation Is Concerning

Broadcom is currently valued at a forward price-to-earnings ratio of 20 in comparison to its 5-year average of 14.4. Although Broadcom seems expensively valued from a historical valuation perspective, I believe we need to cut some slack for the company given how Broadcom has positioned itself to emerge as a big winner of the AI adoption. Even after allowing Broadcom to trade at a premium to its historical valuation levels, I find the company to be valued with no margin of safety for investors today. Even from a price-to-cash flow perspective, Broadcom is richly valued at a multiple of 20.4 compared to the 5-year average of 14.8.

With the VMware acquisition inching closer, I believe we are entering a phase where the company will have to take bold actions to integrate VMware successfully into its business, which might include divesting certain non-core businesses and even layoffs. These actions, although necessary, might end up spooking investors. Given this possibility, I am not comfortable attaching premium valuation multiples that far exceed the quantifiable benefits expected from the growth of AI technology.

Takeaway

Broadcom is well-positioned to grow. The demand environment is encouraging and the VMware acquisition is likely to contribute to growth. Amid all the positives, I am concerned about the company’s current valuation as I believe it leaves me with no margin of safety should Broadcom face a deterioration of investor sentiment in the coming quarters. For this reason, I will wait for a pullback to invest in Broadcom stock.

[ad_2]

Read More: Broadcom Stock’s Valuation Has Outpaced Attractive Fundamentals (NASDAQ:AVGO)

2023-09-04 15:26:56