[ad_1]

JJ Gouin/iStock via Getty Images

UGI Corporation (NYSE:UGI) is reviewing new strategic options. In addition, the company successfully signed new agreements with debt investors, and reported an increase in restructuring costs. Given the beneficial expectations of other analysts and the valuation of peers, UGI looks like a must-follow stock. Yes, there are many risks coming from competition, regulatory challenges, or changes in the retail propane market. With that, I think that UGI right now trades undervalued, and looks like a buy.

UGI Corporation

UGI Corporation, a holding company, stands out for its various business segments. Through AmeriGas Propane, it leads the retail propane market in the US. Its international presence through UGI International encompasses the marketing and distribution of propane and other LPG along with energy services in Europe.

In the Midstream and Marketing segment, UGI is involved in the marketing of energy, midstream infrastructure, storage, and processing of natural gas. Additionally, in the Utilities sector, it manages public natural gas and electricity distribution services as well as natural gas production and electricity generation businesses.

Energy Services leads the retail energy trading business, offering natural gas, RNG, liquid fuels, and electricity to 11,500 customers in more than 41,000 locations throughout the United States. Predominantly, its sales are based on fixed price agreements or exclusive contracts, adapting to customer needs.

Operating primarily in areas without natural gas, the company distributes approximately 940 million gallons of propane annually, serving various sectors and standing out with key services such as ACE and Cynch for home deliveries of propane cylinders.

Recent EPS Normalized Were Better Than Expected, And 6.43% Dividend Yield

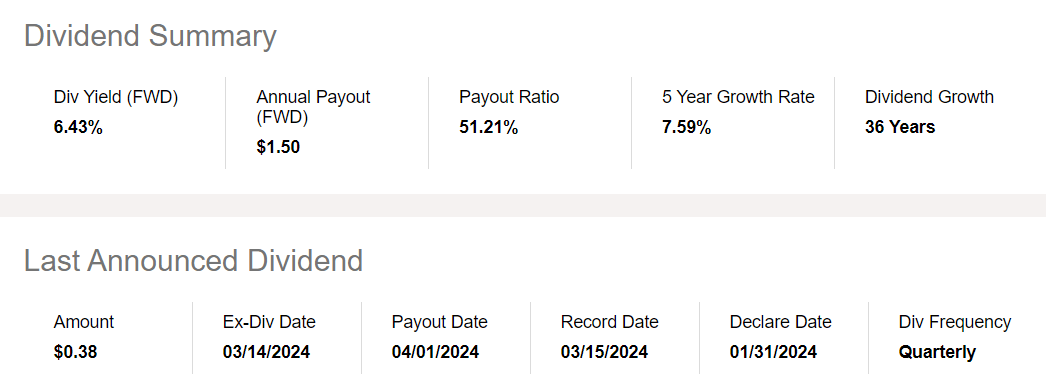

In the last quarterly report, UGI reported EPS normalized better than expected, equal to $1.20. Quarterly revenue stood at $2.12 billion, which was lower than expected. It is also worth noting that UGC has been a dividend aristocrat with 6.43% dividend yield, and a payout ratio of 51%.

Source: Seeking Alpha Source: Seeking Alpha

With that, I think that a quick look at the most recent price dynamics could indicate certain undervaluation. In 2019, UGI was trading at close to $55-$60 per share. Right now, the same company trades at close to $20-$25 per share. Given these price dynamics, I decided to run a valuation model about UGI.

Source: Seeking Alpha

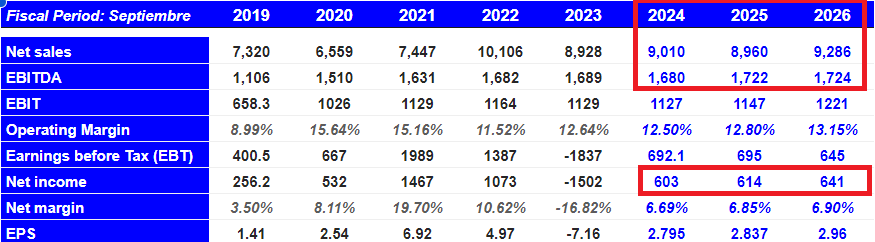

Before reviewing my expectations, in my view, it is worth having a look at the expectations of other investors. Net sales, net income, and net margin are expected to grow from 2024 to 2026. In particular, net sales are expected to be close to $9.286 billion, with 2026 EBITDA of $1724 million, 2026 EBIT of $1221 million, and 2026 net income of close to $641 million.

Source: Market Screener

Balance Sheet

As of December 31, 2023, UGI reported cash and cash equivalents worth $204 million, restricted cash of about $98 million, and accounts receivable of $1188 million. In addition, with accrued utility revenues of about $120 million, inventories worth $441 million, and derivative instruments of $41 million, prepaid expenses and other current assets were $193 million with total current assets of about $2285 million.

Total current liabilities are larger than the current assets, which I do not appreciate. With that, considering the total amount of property and equipment, I believe that banks would most likely offer financing if it is necessary.

The largest assets are property, plant, and equipment worth $8.601 billion, with goodwill of about $3.070 billion. In addition, the company reported intangible assets close to $430 million with total assets worth $15.716 billion. The asset/liability ratio is larger than 1x, so I think that the balance sheet appears healthy.

Source: 10-Q

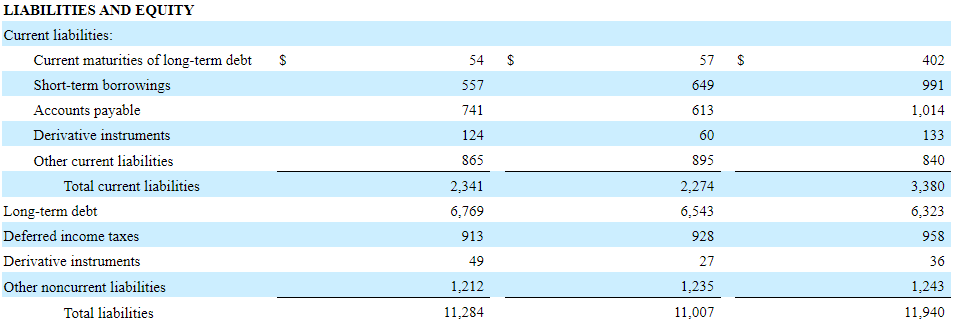

The total amount of long term debt does not appear small, so I believe that investors may want to study it carefully. Current maturities of long-term debt stand at about $54 million, with short-term borrowings of about $557 million, accounts payable worth $741 million, and long-term debt worth $6769 million. Total liabilities stand at about $11.284 billion.

Source: 10-Q

The Strategic Review That Started In 2023 Will Most Likely Bring More Cash In Hand And Lower Debt Levels

UGI promotes its strategy focused on key competencies, such as distribution, storage, and marketing of energy products. With a solid asset base and international experience, the company seeks to accelerate growth organically and through acquisitions.

In 2023, the company initiated a strategic review of the LPG businesses to maximize shareholder value. Its focus is on delivering reliable earnings growth, rebalancing the portfolio toward natural gas and renewable energy, and investing in renewable solutions.

The company highlighted key achievements, such as attractive profit growth in utilities, expansion in renewables in the Midstream and Marketing segment, and progress in the exit of the energy trading business at UGI International.

In my view, the announcement about the strategic review could bring significant interest from institutional investors. In my view, sale of certain assets could bring cash in hand, and lower net debt/FCF, which may enhance UGI’s valuation.

The Company is exploring a full range of options with the goal of reducing UGI’s earnings volatility and strengthening its balance sheet. In conjunction with the strategic review, the Company is also pursuing actions to optimize its cost structure and re-align its capital allocation priorities. The Company continues on its existing plans while the review of strategic alternatives is ongoing. Source: 10-Q

Recent Successful Debt Agreements May Help Reduce Short-term Borrowings

I believe that the recent deal with lenders to refinance the balance sheet as well as to reduce short-term borrowings could bring the attention of debt investors and equity investors. My thesis is that there is demand for the debt, which means that market participants do appreciate the business model. In my view, equity investors may also bring stock demand as soon as the current ratio lowers.

On November 30, 2023, UGI Utilities, Inc. entered into a Note Purchase Agreement with a consortium of lenders. Pursuant to the Note Purchase Agreement, UGI Utilities, Inc. issued $25 million aggregate principal amount of 6.02% Senior Notes due November 30, 2030. The net proceeds from these issuances were used to reduce short-term borrowings and for general corporate purposes. Source: 10-Q

Ongoing Restructuring Could Bring Increases In The Operating Margin And FCF Growth

UGI Corporation appears to be making significant efforts with regard to restructuring costs apart from the sale of divisions in Europe. In my opinion, further efforts and reallocation of resources to profitable assets will most likely lead to improvements in the future FCF margin. As a result, in my view, expectations with regard to future profits could lead to higher stock prices.

Net income attributable to UGI Corporation during the 2023 three-month period also includes restructuring costs largely attributable to a reduction in workforce and related costs. Source: 10-Q

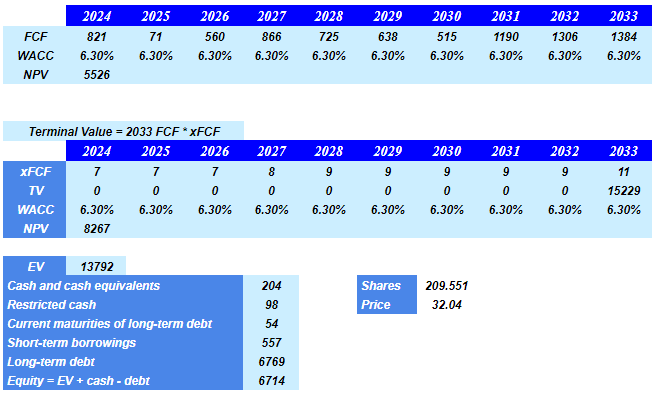

My FCF Expectations Based On Previous Cash Flow Statements And My Own Assumptions

My expectations include net income of close to $891 million, with 2033 depreciation and amortization worth $780 million, deferred income tax expense of about -$78 million, and changes in unrealized gains and losses on derivative instruments worth $240 million.

Besides, my expectations also include equity-based compensation expense of about $3 million, losses from equity investees worth -$300 million, 2033 changes in accounts receivable and accrued utility revenues worth $125 million, and changes in inventories close to $213 million

In addition, with changes in accounts payable worth -$403 million and changes in other current liabilities of about -$63 million, 2033 net cash provided by operating activities would stand at $2584 million. Finally, with expenditures for property, plant, and equipment worth -$1200 million, 2033 FCF would be close to $1.384 billion.

Source: Dahlia Investments

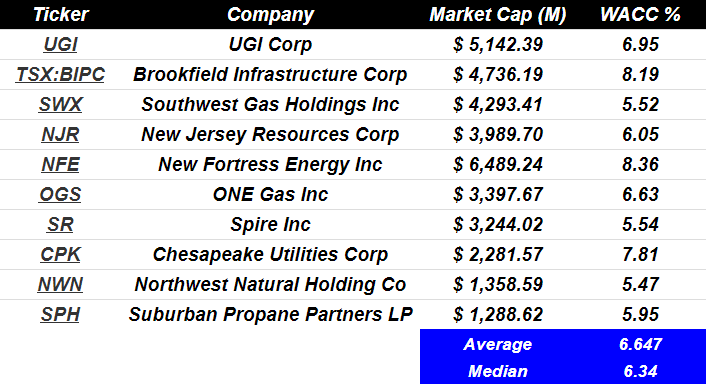

Other analysts out there included a WACC for competitors between 5% and 8%, with an average of 6% and a median of close to 6%. Seeking Alpha reports a median cash multiple in the sector of 7x and EV/EBITDA of 12x. With these figures, I assumed an exit multiple of 11x FCF, which I believe is conservative.

Source: Gurufocus Source: Seeking Alpha

My results include a net present value of future FCF of $5 billion, NPV of future terminal value close to 11x, and total implied enterprise value of $13.7 billion. Now, if we add cash in hand and subtract the total amount of debt and short-term borrowings, the implied price stands at close to $32 per share.

Source: Seeking Alpha

Risks

In my opinion, the LPG industry has experienced no or modest growth, predicting that annual volumes will depend mainly on weather patterns. Its growth capacity is tied to acquisitions and internal programs, such as ACE, Cynch, and national accounts. State and federal regulatory oversight, along with obtaining property rights and approvals, presents challenges. Opposition from various groups could affect the expansion of assets. Failure to retain and acquire customers as well as complete infrastructure projects may have adverse consequences on our financial condition and operating results.

Competitors

In my opinion, the market in which the company operates faces intense competition, mainly with energy sources such as electricity, fuel oil, and natural gas. Although electricity is more expensive in terms of Btu equivalent, its convenience makes it attractive. Fuel oil, despite being less environmentally attractive, competes with propane. In areas without natural gas, propane serves as an alternative. For motor fuels, it…

[ad_2]

Read More: UGI: Strategic Review, Recent Debt Agreements Are Positives

2024-02-12 19:08:23